Claims Matrix FAQs

Visit Matrix > Claims for a comprehensive view of your claims.

Visit this report daily to e-File or print claims, address unpaid claims, and to find claims needing more information. Here are some commonly asked questions about the Tops Ortho Claims Matrix.

Questions:

🐜 Bug Alert

The All Delinquent Claims view in the Claims Matrix should include open claims with a status of Clearinghouse Accepted or Clearinghouse Rejected; however, there is a current issue that excludes qualified claims with these statuses fro the report.

This is a known issue and will be resolved in a future Tops update.

Workaround: Use one of the following views until the issue is resolved:

- Unpaid Claims with the Open Claims Only filter applied, then sort by Date or Aging.

- All Claims in the Last 120 Days with the Open Claims Only filter applied (for claims 120 days old or less)

- Delinquent Submitted Claims

Note: Delinquent Submitted Claims and All Delinquent Claims will not include claims older than 120 days or claims with a calculated payment value.

What is the Claims Matrix?

The Claims Matrix is a centralized view of insurance claims in Tops and is primarily used to manage open claims. Claims can be searched and reviewed by Status, Category, Date Range, Submission Value, Office and other filters. Most practices use the Claims Matrix to:

- Review claims awaiting payment.

- Identify claims that need to be submitted electronically or by paper.

- Monitor claims requiring attention due to missing information or submission issues.

- Track aging claims and follow up on outstanding insurance payments.

Claims are generated based on qualifying ledger activity and the settings configured within the patient’s Employer Policy. Qualifying ledger activity includes transactions designated to appear on insurance claims, such as contract charges, treatment fees, and other insurance-billable transactions.

The Employer Policy determines when and how claims are generated through settings such as Claim Frequency, Claim Type and Payment Calculation.

Example: If an Employer Policy is configured with a One-Time Only submission, and a Quarterly claim payment frequency, and has a Next Claim Date of 4/1/2026, Tops reviews qualifying ledger activity posted since the previous claim period and generates a Payment Reminder claim containing those transactions. This may include automatically posted contract charges as well as manually posted fees designated to appear on insurance claims.

Search by Category

The Category filter determines which group of claims is displayed. Additional filters, such as Status, Submission Value, and Office, can then be used to further narrow the results.

Unsent Ready-to-File claims

Claims that are ready to be submitted. This includes automatically generated initial claims, claims that require submission for payment, pre-estimates that have been completed, and date range claims that require submission.

Unsent Missing-Info Claims

Claims that cannot be submitted because required information is missing or incomplete. Hover over the caution icon (⚠️) to identify the missing information. Once corrected, the claim moves to Unsent Ready-to-File claims.

Unsent PreEstimate Claims

Manually created pre-estimate, pre-determination, or pre-authorization claims that have not yet been submitted.

Unpaid Claims

Displays all claims that have not been updated to a Paid status. Use the Status filter to narrow the list.

All Delinquent Claims

Displays unpaid claims that meet the delinquent claim criteria. To appear in this view, a claim must:

- Be 120 days old or less.

- Have an assigned Possible Payment value.

- Be an automatically generated or initial claim.

Use the Status filter to review Open Claims.

Delinquent Submitted Claims

Displays delinquent claims that remain open and have either a submission date or are designated as Payment Reminder claims. These claims meet the same delinquent claim criteria as All Delinquent Claims.

Sent Billing-Only Claims in a Date Range

Displays submitted Billing-Only claims within a selected date range. Because payment is expected to be sent directly to the patient rather than the practice, these claims automatically close after submission. For best results, use the Closed Claims Only status filter.

Paid Claims in a Date Range

Displays claims marked as Paid within the selected date range.

All Claims in the Last 120 Days

Displays all claims generated within the last 120 days, regardless of status. Use the Status filter to view only Open, Paid, Closed or Voided claims. Use the Submission Value filters to further refine results.

All Claims in a Date Range

Displays all claims generated within the selected date range, regardless of status. Use the Status and Submission Value filters to further define the results.

Why can't I see my Unpaid Claims?

Don't worry-you still can! When you select the Unpaid Claims filter in the Claims Matrix, Tops Ortho defaults to showing you the claims in Rejected by Clearing House status. This is because these claims require your prompt attention.

To see all of your Unpaid Claims, set the filters from left to right to:

- Unpaid Claims

- All Offices (or the office of your choice)

- All Submission Values

- Open Claims Only

Why don't all open claims reflect a payment value?

A claim’s possible payment value is determined by the patient’s remaining policy benefit and the payment calculation configured in the Employer Policy. As a result, not every open claim will display a possible payment value.

A claim may display $0, a question mark (?) , or no value for any of the following reasons:

- The patient’s remaining policy benefit has already been allocated to older open claims.

- The patient has no remaining benefit available on the policy.

- The claim is a manually generated date-range claim, which is not assigned a possible payment value.

- No payment percentage has been configured in the Employer Policy, causing the claim to display a question mark (?) or no value.

- The claim is more than 120 days old. Possible payment values are displayed only for claims within the 0-120 day aging period. (Due 90+ represents the final range of 91-120 days).

- Although claims older than 120 days no longer display a possible payment value, any benefits previously allocated to those claims remain reserved. Those reserved benefits continue to be considered when calculating possible payment values for newer claims.

Example

A patient has:

- $400 of remaining policy benefits

- A 50% payment calculation

- Five open claims, each with $200 of eligible charges

Tops allocates the available benefit beginning with the oldest claim. The first four claims each receive a $100 possible payment value, exhausting the available $400 benefit. As a result, the fifth claim displays $0 because no remaining benefit is available.

If one or more of the first four claims are more than 120 days old, they will no longer display a possible payment value in the Claims Matrix. However, the benefits allocated to those claims remain reserved and are therefore unavailable to newer claims.

Important: A claim’s possible payment value is calculated using the Employer Policy’s remaining benefit and payment calculation settings. It is not based on the patient’s Expected Insurance balance.

Why did the payment value of my open claims change?

The payment values displayed in the Claims Matrix are recalculated whenever changes affect the patient’s remaining policy benefit or the amount of an open claim. Common reasons include matching insurance payments to claims, manually closing open claims, or modifying contract charges.

Matching a Payment to a Claim or Manually Closing an Open Claim

When an insurance payment is matched to a claim, or an open claim is manually closed, Tops may recalculate the remaining policy benefit across the patient’s other open claims. For example, if a single insurance payment satisfies charges that were originally represented by multiple open claims, manually closing the remaining related claims may reallocate available policy benefits to the patient’s other open claims. This can change the possible payment values displayed in the Claims Matrix without affecting the patient’s Expected Insurance balance.

Modifying the Amount Column in the Contract Worksheet

Updating the Amount column changes the periodic contract charges that are posted to the patient’s ledger. Because automatically generated claims are created from qualifying ledger transactions, future claims will reflect the updated charges. As a result, future claim amounts- and therefore their possible payment values-may change based on the updated charges, the Employer Policy’s payment calculation, the patient’s remaining benefit, and other open claims.

Note: Changes to payment values in the Claims Matrix do not affect the patient’s Expected Insurance balance. Expected Insurance and Claims Matrix payment values are calculated independently.

Why does my claim's aging reflect a question mark (?) ?

If a claim payment value reflects a question mark, it is due to the Employer Policy missing the payment percentage.

My claim is older than 3 months. Why is there not a value represented in 90+?

Tops will only show an estimated payment value with an open claim if the claim is between 0 and 120 days old. The age of the claim is based on the claim generate date, the first date represented in the claims matrix. The 90+ column represents a claims age of 91-120 days.

- Please reference the questions regarding payment values here.

My claim is less than 4 months old. Why is there not a value represented?

- Date range claims do not display estimated payment values.

- Please reference the questions regarding payment values here.

Why do I not see ALL of my claims that are over 30 days old in my All Delinquent Claims view?

All open claims that appear in the All Delinquent Claims view will also appear in Unpaid Claims view with the Open Claims Only filter selected. The reverse is not true. All claims over 30 days old in the Unpaid Claims>Open Claims Only view do not appear in the All Delinquent Claims view.

Claims in the matrix are aged by generation date in the following ranges: 0 to 30, 30 to 60, 60 to 90, and Due 90+ (Due 90+ representing the final range of 91-120 days).

The All Delinquent Claims view provides visibility to only those claims that meet the following requirement:

- The claim is between 31 and 120 days old.

- The claim displays a possible payment value.

- The payment value displayed for a claim is based on the benefits remaining on the patient’s policy. Tops first allocates any available benefits to older, open claims, regardless of age. If benefits remain after those claims are considered, Tops applies the employer policy’s payment percentage to calculate the estimated payment amount for the current claim and displays the remaining benefit available to pay that claim.

- Date range claims are never assigned a payment value and therefore, will not appear in you Delinquent Claims list.

- Claims that remain open beyond 120 days will still appear in the Unpaid Claims Matrix under Open Claims Only, but no longer will display a possible payment value or appear on the Delinquent Claims list.

Why did a new claim appear or disappear on my Delinquent Claims view?

New Claim Appeared

Tops calculates potential payment values by applying the remaining benefits available on the policy to open claims, starting with the oldest claim first.

In some cases, an older claim may consume all available remaining benefits when Tops calculates potential payment values. As a result, newer claims may not display any payment value because no benefits remain available for them.

Once a payment is posted to that older claim, the claim is closed and no longer reserves its previously calculated payment value. Tops then recalculates the remaining benefits available on the policy and applies them to the next oldest open claims.

If one of those claims now calculates a potential payment value and falls within the Delinquent Claims criteria (older than 30 days but not older than 120 days), it will appear on the Delinquent Claims view.

In short, posting a payment to an older claim can free up available benefits for other open claims, causing those claims to calculate a payment value and become visible on the Delinquent Claims report.

Existing Claim Dropped off List

When a claim is "matched" with an insurance payment, the status will update to "paid" and it no longer remains open. If it was on the Delinquent list, it will now no longer appear.

If there is no more benefit remaining on the patient's policy to pay the open claim, the claim will no longer appear on the Delinquent list.

Additionally, if a claim ages out of the Delinquent Claims list, it means the claim is older than 120 days old. The claim will drop off the Delinquent Claims list but still appear in your Unpaid Claims>Open Claims Only view.

What is the difference between the two views, Delinquent Claims and Unpaid Claims>Open Claims Only? How should they be utilized?

All open claims that appear in the All Delinquent Claims category will also appear in Unpaid Claims category with the Open Claims Only filter selected.

**The reverse is not true. **

All claims over 30 days old in the Unpaid Claims>Open Claims Only view do not appear in the All Delinquent Claims view.

The Open Claims Only filter of Unpaid Claims is the best option when:

- You have claims that may be older than 120 days.

- You are cleaning up a congested Claims Matrix containing old or unnecessary claims.

- You want to review all open claims regardless of age or calculated payment value.

The All Delinquent Claims view is most effective when your practice actively manages all open claims and has few or no open claims older than 120 days. Because claims older than 120 days are excluded from this view, practices with a significant number of older open claims should use Unpaid Claims>Open Claims Only to ensure no outstanding claims are overlooked.

Should Expected Insurance on my Accounts Receivable match the Claims Matrix claim payment totals?

No. Expected Insurance on the Accounts Receivable report and the claim payment amounts shown in the Claims Matrix are calculated independently and are not intended to match.

- Expected Insurance is a ledger-based value that represents the portion of a patient’s balance expected to be paid by insurance.

- The Claims Matrix is claim-based and calculates claim payment amounts using the Employer Policy’s remaining benefit, payment calculation, and existing open claims.

Because these values are calculated differently, their totals will not reconcile.

Understanding Expected Insurance

Expected Insurance represents the portion of a patient’s total balance anticipated to be paid by insurance. The value displayed on the Accounts Receivable report is the same Expected Insurance amount shown in the patient’s chart. It is derived directly from the patient’s ledger and is used to distribute the patient’s balance among Due Now, Future Due, Copay and Expected Insurance.

Expected Insurance changes as ledger activity occurs, including:

- Creating an initial contract with insurance, when a portion of the treatment fee is designated as Expected Insurance.

- Modifying an insurance contract by increasing or decreasing the Expected Insurance amount in the Contract Worksheet.

- Posting a fee in the Transaction Window and assigning a portion of the fee to Expected Insurance.

- Posting an insurance payment to the patient’s ledger.

- Manually adjusting Expected Insurance using Action>Change Expected Insurance.

Because Expected Insurance is calculated from ledger activity, it is not tied to individual claims or to Claims Matrix payment amounts.

Relationship to the Claims Matrix

The Claims Matrix calculates claim payment amounts independently of Expected Insurance. Changes to one system do not automatically affect the other.

For example:

- Changing Expected Insurance does not change an Employer Policy’s remaining benefit or the payment amount shown on open claims.

- Adjusting an Employer Policy’s remaining benefit, closing a claim, or voiding a claim does not change the patient’s Expected Insurance balance.

Certain events can affect both Expected Insurance and the Claims Matrix. Although these events may impact both systems, each recalculates independently.

Posting an Insurance Payment

- Reduces the patient’s Expected Insurance balance on the ledger.

- Reduces the Employer Policy’s remaining benefit associated with that payment.

Although these actions may affect both systems, they do so independently. Expected Insurance is derived from the patient’s ledger, while Claims Matrix payment values are calculated using the claim amount, the Employer Policy settings, the patient’s remaining benefit, and any other open claims. For this reason, the two totals are not intended to match.

|

|

What can you see from this snapshot? Expected Insurance - $23.12 Remaining Benefit on the policy - $400.00 Make Claims Automatically - Checked Next Claim Date - Future Date Active Contract - No • Expected Insurance is not tied to the Remaining Benefit • The contract is no longer active. Periodic claims will no longer generate based on the contract. • Tops will continue to look for ledger transactions that qualify for claims and generate a claim on the next claim date. Make Claims Automatically is checked and there is a future, next claim date. |

How should I address my aging claims?

A good way to manage aging claims is to review the Claims Matrix and Accounts Receivable Report together. The Claims Matrix identifies open claims, while the Accounts Receivable Report shows whether the patient is still expected to receive an insurance payment.

Step 1: Review Open Claims

In the Claims Matrix, select the Unpaid Claims category and apply the Open Claims Only status filter. Sort the list by Patient Name to make it easier to compare with the Accounts Receivable Report.

Step 2: Cross Reference the Accounts Receivable Report

Review patients with an Expected Insurance balance. For easier review, move the Last Ins Pmt Amount and Last Ins Pmt Date columns so they appear next to the Expected Insurance column.

As you review each patient, ask:

- Does the patient still have an Expected Insurance balance?

- Has an insurance payment been posted recently?

- If a recent payment was received, why are multiple claims still open?

- If no payment has been received, is follow-up with the insurance carrier needed?

Step 3: Review Unnecessary Open Claims

If a patient has open claims but no remaining Expected Insurance balance, review the patient’s chart to determine why the claims remain open.

Depending on your findings, you may need to:

- Close or void unnecessary claims (individually or in bulk).

- Edit and resubmit claims that require correction.

- Review the Employer Policy to verify the claim generation or submission frequency.

- Update the claim frequency or submission settings, recalculate the Next Claim Date, and close unnecessary open claims.

- If claims are no longer needed, uncheck Make Claims Automatically, remove the Next Claim Date, and close or void the remaining open claims.

Step 4: Review the Oldest Claims

After reconciling the Accounts Receivable Report, review any remaining open claims by sorting the Claims Matrix by Date (the far left column). The date represented is the generation date of the claim.

Focus first on the oldest claims. Claims approaching one year old may be nearing timely filing limits. Establish an internal policy for how long your office will keep unresolved or unnecessary claims open, then use Edit>Void Selected Claims to void claims that are no longer valid.

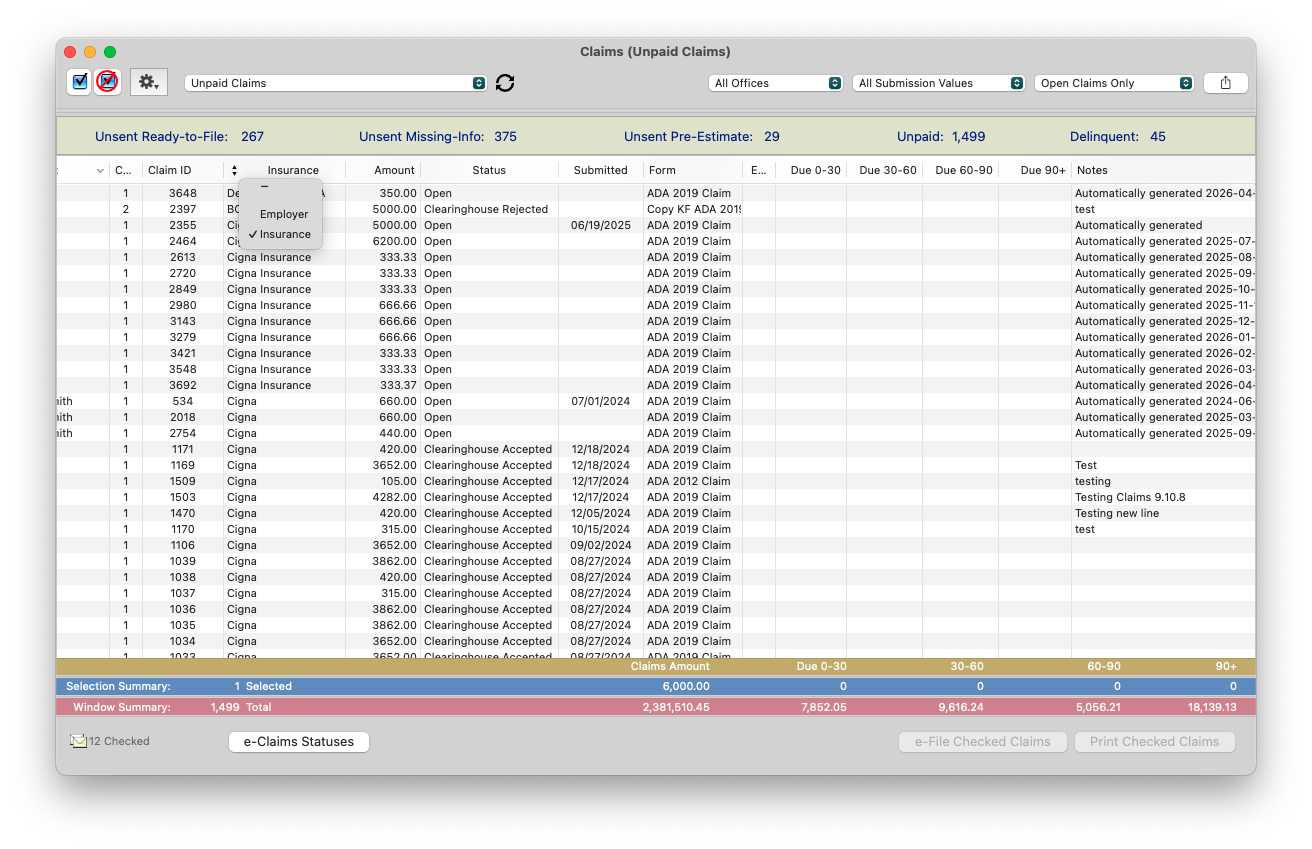

Can I view this report by Insurance Company?

Yes!

- Simply click the up/down arrow icon on the Employer heading and select Insurance instead.

-

Click the Insurance heading to group Insurers together.

What do the symbols in the second column mean?

These are indicators of claim type:

- A dot indicates an Initial Claim

- A diamond indicates a Pre-Estimate/Pre-Determination Claim

- No indicator present indicates a Periodic or Date-range Claim.

What does the yellow caution sign (⚠️) mean?

A yellow caution sign (⚠️) indicates that the claim contains missing, incomplete, or invalid information.

Tops automatically checks claims for required information when they are generated. If information is missing, a ⚠️ appears next to the claim in both the Claims Matrix and the patient’s Claims tab.

Hover over the ⚠️ to view the specific error message and identify what information needs to be corrected.

If the claim status reflects 'Open'

The claim is missing information required for submission.

-

Hover over the ⚠️ to view the missing details.

Update the patient, policy holder, employer policy, or other referenced records as directed.

If the error specifically instructs you to edit the claim, you'll need to update the details in the places identified. To edit details in the claim, right-click the claim and select Edit Claim to update the claim record with the instructed correction.

- Example fields that require updates in the claim: Assignment of Benefit, Treatment Phase, Dental Classification, Pre-Determination Authorization code, Coordination of Benefits primary payment details.

- Refresh the Claims Matrix after making corrections.

These claims can be found in:

Matrix>Claims>Unsent Missing-Info Claims

Once all errors are corrected, the claim is ready to be submitted.

If the claim status reflects 'Clearinghouse Rejected'

The claim was submitted but was rejected by the clearinghouse due to validation errors.

- Hover over the ⚠️ to view the rejection reason.

- Correct the information indicated in the error message.

- Refresh the Claims Matrix from the Unpaid Claims>Rejected by Clearinghouse view.

These claims can be found in:

Matrix>Claims>Unpaid Claims>Rejected by Clearinghouse

For additional guidance, see referenced articles:

- eClaims with Rejected by Clearinghouse Status

- Common eClaim Rejection Reasons

What information pulls in the Notes column?

- This column displays what is typed in the Internal Notes for this Claim field.

- To view or edit this field, right-click on the claim and select Edit Claim.